Financing your first small business acquisition to make >$200k a year

A simple deal example that would allow you quit your job and make $200k a year with only $30k out of pocket

Welcome 546 of you new readers since my last post!

Thank you so much for following a long.

If you’re new, I’m building & acquiring small businesses as a lifestyle entrepreneur.

This means, I’m designing my work around my life.

Work is NOT life.

Rather, how can work be part of what matters to me: My wife and kids. My physical, mental and emotional health and friends / family.

I’m not out to build a unicorn. But I enjoy the chase of money.

So, my goal is to build a small holding company that owns multiple small businesses that net over $1M a year in EBITDA.

After today, we’ll be driving much closer to that number 😉

Follow a long for some upcoming news…

Let’s dive in…

_________

The number 1 question I get is about financing.

‘How do you actually afford to buy a small business’…

I’m convinced most people tell themselves, “I can’t afford a small business” and don’t even start to look.

Well, I’m here to break down a deal and show you how to buy a small business, quit your job and own 100% of a small business where you can make $200k a year and work for yourself.

Before I dive in I want to be clear about a few things:

I’m making some assumptions here as I know nothing about this deal except what is posted here

I’m NOT an expert in structuring a deal by any means. My goal here is to show you one of the most simplistic ways to finance a small business. I believe most people won’t even start down this path because of this single hang up, ‘how could I afford it’

This is not financial advice. Maybe it’s not even good advice. It’s simply not advice… it’s just how I would think about (am an doing a deal just like this as we speak)

There’s a million different ways to finance a deal. This is a really straight forward example in hopes to get you past the ‘I can’t afford to buy a small business’ phase and start looking…

Here’s the deal:

This was some random deal that caught my eye on Bizbuysell.

3 things that catch my eye scrolling through all the bizbuysell ads?

Cashflow: $409k. With this kind of cashflow, I can finance a deal and usually the numbers will pencil out well

Asking Price: It’s only 2x EBITDA. Pretty damn cheap. Most SMBs will sell between 2x-5x cash flow.

Gross Revenue: At $1.5M, they are operating at ~27% margins. Not amazing, but decent. My assumption is always that I can improve margins a bit with tech, automation, etc.

Assuming these numbers are accurate (not always are they accurate once you get the CIM and dive into P&Ls)… here’s 1 option of how these numbers could pencil out.

Remember, this is a pretty simplistic model:

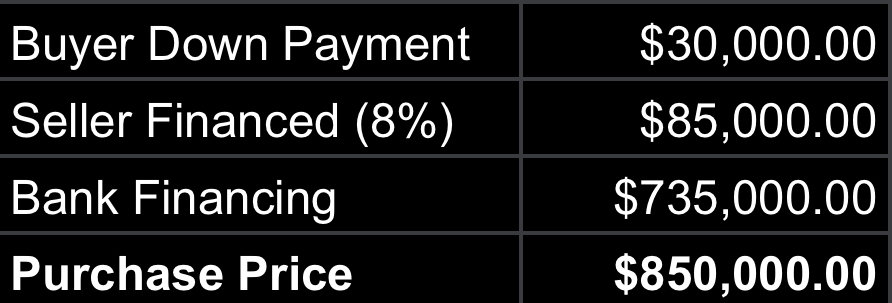

Buyer Down Payment:

If you’ve saved up $30,000, this would become your down payment. With the new SBA rules, this wouldn’t even be necessary if the seller did at least 10% of the deal seller financed.

Regardless, there’s many ways to come up with the $30,000. Save cash, take out a HELOC, take a loan against your 401k, give up some equity and raise the $30,000 from your grandma, etc…

Seller Financing:

I’ll pretend that the seller agreed here to do 10% seller financing at 8% interest rate for 5 years. This would provide the seller no less than $1,723 a month of income from you as the new business owner for the next 5 years.

It’s not a bad option for sellers if they aren’t looking for the cash right now…

Bank Financing

I’m going to assume you’ll be quitting a W2 job and getting a SBA loan (one the best options if you haven’t worked for yourself for over 2 years or have a huge amount of assets in your name already). I haven’t personally gone through the SBA process but I’ve begun it and talked to many that have gone through it.

Regardless, we’ll assume a 10 year loan at a 11% interest rate which is close to what it is right now.

The point here isn’t to dive into the SBA, it’s to show you how this deal would pencil out.

The Details:

Assuming operating expenses stay the same and net margin is at 27%:

In this scenario, you’d net $267,672 a year.

You could invest another $60k+ each year to pay down debt service to payoff the business sooner.

If you didn’t grow the business at all and threw the $60k a year to pay off your debt, you could own the business outright in just over 5 years…

Now think about that…

You can own an asset that now cash flows >$34k a month to you (>$400k a year) that you own 100% of. Mind you, the business itself is worth ~$1M if you were to sell it.

Not a bad option compared to a W2 IMO.

Don’t be afraid of the financing… it’s not as hard or as complicated as I thought it would be.

For what it’s worth, even if you didn’t have the $30,000 to put down and you used the 10% seller financing as your ‘down payment’ for the SBA loan, this deal will still cashflow in a similar way.

There’s obviously more to a deal and likely more capital required to grow, run the business or even maintain sometimes… but don’t let those things hold you up.

Hope this can shed some light on a simple way to potentially finance a deal and encouraged someone to try.

Know someone looking to acquire but stuck before getting started? I’d be honored if you’d share this with them!

I’m closing an a 2nd acquisition today. I’m funding a small portion of it from my earnings this year as a consultant where I work as a contractor for multiple companies. It’s arguably one of the most lucrative jobs someone could do.

I began consulting in January of this year and scaled it to >$40k a month with 98% margins. I’ve packaged up all my learnings into a course. I believe most of you that want to try your hand at building a service business as a side hustle, can.

I believe you should.

Because in the world we live, you never know when your income will get cut off.

If your employer decided they don’t need you anymore, you’re income could be gone over night.

Use code: FRIEND50

and get it here for only $99 now.

I’m going through this process now. Company price $890k, 3x multiple. SBA lenders are looking for more personal liquidity than you mention, even if the seller is willing to do a 10% note. They are wanting me to have 10% post close liquidity on hand AFTER being able to cover 10% down. So essentially 20%. I’m sure it’s temporary based on the current climate, but this is what I’ve seen from multiple SBA lenders so far.